3D Animation Software Market: By Technology (3D Modelling, Motion Graphics, 3D Rendering, Visual Effects, Others); Deployment (On-Premises, Cloud); Application (Animation Field, Media Field, Construction Field, Others); End-Users (Media & Entertainment, Construction & Architecture, Healthcare & Lifesciences, Fashion & Textile, Education & Research, Others); Region—Market Size, Industry Dynamics, Opportunity Analysis And Forecast For 2025–2033

- Last Updated: 13-Nov-2025 | | Report ID: AA0623475

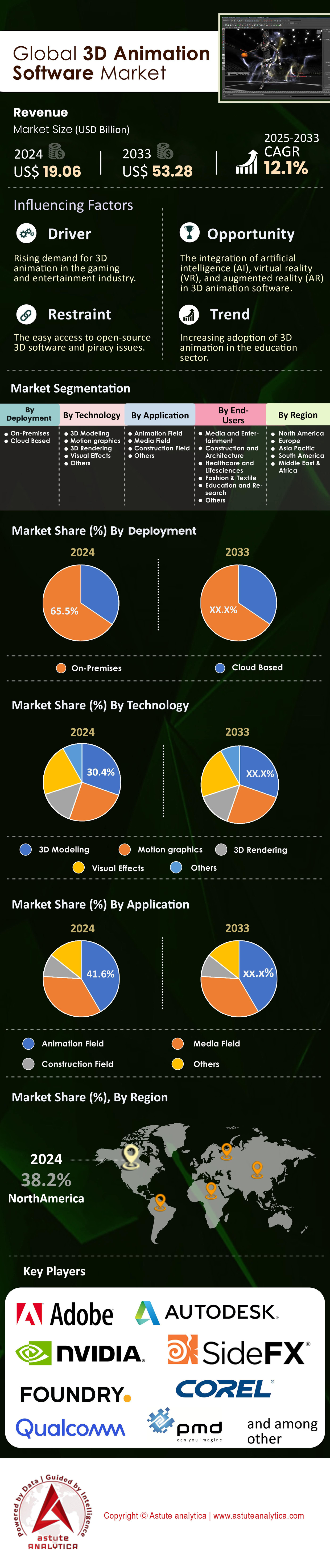

Market Snapshot

3D animation software market generated a revenue of US$ 19.06 billion in 2024 and is projected to reach valuation of US$ 53.28 billion by 2033 at a CAGR of 12.1% during the forecasted period 2025-2033.

Key Findings

- By deployment, cloud-based deployment of 3D animation software accounted for the highest market share of 66.5%.

- Based on technology, 3D modeling technology is currently leading the 3D animation software market and is controlling the largest 30.4% revenue share.

- Based on application, the 3D animation software heavily used in the animation Field and accounts for 42.3% market share.

- Based on end users, media & entertainment industry held the largest segmental share of 40.4%.

- North America is leading the global market by capturing the highest 38.20% market share.

A fundamental shift from static content to interactive experiences is redefining the entire 3D animation software market. The demand is no longer just for pre-rendered videos but for dynamic, real-time applications that are reshaping workflows across industries. This transformation is attracting serious capital, evidenced by a new US$ 500 million virtual production hub beginning construction in Canada. This facility is designed around cutting-edge hardware, including massive 60-foot by 20-foot LED walls and 4K OLED displays. To further catalyze development, Singapore has established a US$ 22.4 million co-production fund. Parallel to these investments, artificial intelligence is automating complex processes. Autodesk's acquisition of Wonder Dynamics in May 2024 is a clear signal that major players are betting on AI, which is already delivering results like a 40% reduction in motion capture setup times.

The 3D animation software market's expansion into new commercial and industrial sectors is creating powerful new revenue streams. In e-commerce, 3D assets have become a vital tool for engagement, with shoppers spending an average of 20 seconds interacting with a 3D product view. This deeper connection has a direct financial benefit, as the implementation of 3D viewers can reduce product returns by an impressive 40%. The manufacturing sector represents another major frontier, with industry leaders like General Motors using digital twins to simulate entire production lines. The efficiency gains are enormous, offering the potential to slash product development times by 50%. Tying these diverse applications together is a universal demand for greater realism, with 8K rendering quickly becoming the new standard.

Fueling this broad adoption is the remarkable accessibility of powerful tools, which is democratizing content creation in the 3D animation software market. Open-source software is at the forefront of this movement; in late 2024, nearly 10,000 people were using Blender on the Steam platform at any given moment, and the software's official site saw around 60,000 downloads daily. This growth is supported by a robust community, with Blender's Extensions Platform now hosting over 300 add-ons. This grassroots explosion is creating a vast, skilled talent pool. The value of these new skills is reflected in the job market, where roles requiring real-time engine expertise now command an average salary premium of US$ 14,354, signaling a vibrant and opportunity-rich future.

To Get more Insights, Request A Free Sample

Unlocking Future Realities and AI-Driven Creation in the Animation Market

Significant opportunities are emerging for players in the 3D animation software market who can capitalize on nascent but powerful technological shifts. These trends promise to redefine content creation workflows and lower the barrier to entry for professional-quality 3D asset generation.

- Generative AI for Text-to-3D Creation: A transformative opportunity lies in integrating generative AI models that create 3D assets from simple text prompts. Tools like Luma AI's Genie and NVIDIA's platform are moving from research to practical application, allowing designers to rapidly prototype ideas without complex modeling skills. Software providers that successfully build intuitive, AI-powered asset generation features directly into their platforms will capture a new segment of users, dramatically accelerating content creation for games, the metaverse, and product design.

- Neural Radiance Fields (NeRFs) Integration: An equally compelling frontier is the adoption of Neural Radiance Fields for 3D scene capture. NeRFs use AI to construct photorealistic 3D environments from a handful of 2D images or a short video clip. The opportunity for the 3D animation software market is to develop tools that can import, edit, and render NeRF data. Doing so will enable creators to produce unparalleled digital twins, hyper-realistic e-commerce visualizations, and seamless VFX shots with a fraction of the traditional effort.

Building Persistent Digital Worlds Drives Demand for Interoperable 3D Assets

A new kind of digital frontier is taking shape, creating an urgent and specialized need within the 3D animation software market. We are witnessing the rise of a powerful creator economy, where software empowers users to build persistent, shared worlds. Platforms like Roblox are at the forefront, paying out a staggering US$ 741 million to its community of creators in 2024 alone. These developers, in turn, built over 7 million new experiences for others to explore. The value of these spaces is tangible, with more than 150,000 parcels of virtual land sold across major platforms. It's a movement attracting serious talent, as NVIDIA's Omniverse platform saw its active developer count swell past 400,000. Brands are not just observing; they are participating, launching over 1,200 unique brand activations to meet users where they live digitally.

This explosion of creativity hinges on software that supports collaboration and open standards. The push for interoperability is clear, with over 350 major companies in the 3D animation software market contributing to the development of the OpenUSD framework in 2025. Digital identity and self-expression are cornerstones of these worlds, driving the sale of more than 2.5 million unique virtual apparel items in 2024. Entertainment has also found a new home here, with over 400 major virtual concerts drawing millions of attendees. All of this activity powers a thriving market for virtual goods, with transaction volumes estimated to hit US$ 1.8 billion in 2025. Ultimately, it all comes back to the individual, with over 1.5 million unique, interoperable avatars created to travel across this emerging digital landscape.

Hyper-Realistic Simulation for AI Training Redefines Industrial Software Needs

Beyond entertainment, a critical demand is emerging from the world of autonomous systems, pushing the 3D animation software market into new territory. The AI that powers self-driving cars and advanced robotics learns in virtual worlds, requiring photorealistic, physics-based simulations. The scale of this digital training is immense; autonomous vehicle developers like Waymo collectively logged over 30 billion simulated miles in 2024. To meet this need, platforms like NVIDIA's DRIVE Sim can now generate 100,000 unique traffic scenarios every hour. The investment is massive, with the U.S. Department of Defense awarding US$ 850 million for military training simulations in 2024. This has created a fierce demand for talent, with over 8,000 new simulation engineer roles posted in 2025.

These virtual training grounds require software capable of incredible precision and data management. They are not just visually complex but data-rich, with a single autonomous vehicle company generating over 40 petabytes of simulation data in 2024. The applications in the 3D animation software market are broadening quickly, with more than 30 major global cities commissioning digital twins by 2025 to simulate traffic and emergency response. The need for accuracy is absolute, as leading robotics firms in 2024 require simulation accuracy to within 2 millimeters of reality. In manufacturing, over 500,000 factory floor layouts were simulated in 2025 to perfect robotic workflows. The aerospace industry is just as reliant, creating over 200,000 flight simulation variables, proving that this demand is for verifiable, data-driven truth.

Segmental Analysis

Cloud-Based Solutions Power a Revolution in the Animation Industry

The shift toward cloud-based deployment has fundamentally reshaped the 3D animation software market landscape, with these solutions now accounting for the highest market share of 66.5%. This dominance is a direct response to the industry's need for greater flexibility and remote collaboration, a trend massively accelerated by the global pandemic. With 63% of companies now operating on hybrid or fully remote models as of 2025, cloud infrastructure has become the backbone of modern production pipelines. Consequently, artists and directors can collaborate seamlessly in real-time across continents, transforming the cloud from a mere convenience into an essential tool for maintaining business continuity and accessing a global talent pool.

These operational advantages are complemented by significant financial benefits, further solidifying the cloud's leading position in the 3D animation software market. For instance, cloud-hosted generative AI tools are poised to reduce production costs by a remarkable 30%, while real-time rendering technologies can shorten animation production timelines by up to 40%. Underscoring this trend, investments in cloud rendering solutions surged by over 38% in 2024. The number of VFX projects rendered in the cloud grew from 15,000 in 2023 to 28,000 in 2024 and is forecast to surpass 75,000 by 2032, democratizing access to powerful computing resources for studios of all sizes.

- Between 2023 and 2024, over 40 new VFX studios were established globally, many adopting cloud-native workflows from their inception.

- Federal media grants under the 2024 Digital Entertainment Act in the U.S. have designated US$ 350 million for cloud-based VFX innovation hubs.

- Global investment in expanding VFX infrastructure exceeded US$ 6.8 billion across 2023 and 2024, with a large portion funding cloud capabilities.

3D Modeling Technology Forges the Future of Digital Content Creation

3D modeling technology is the cornerstone of the industry, currently controlling the largest revenue share at 30.4%. Its leadership is cemented by its foundational role in creating every digital asset, character, and environment seen in modern animated content. The relentless pursuit of photorealism and immersive experiences in films, video games, and virtual reality continuously drives the need for more sophisticated 3D modeling tools. The integration of artificial intelligence is amplifying this effect, as AI-driven features automate complex processes and accelerate creative workflows. As a result, investments in 8K rendering and particle-level detailing have become common, reinforcing the critical importance of advanced 3D modeling within the 3D animation software market.

Furthermore, the application of 3D modeling is rapidly expanding into burgeoning sectors, securing its market dominance. The augmented and virtual reality market, which is projected to reach US$ 46 billion in 2025, relies heavily on 3D animation to build its interactive worlds. In the gaming sphere, the market for 3D game art services is set to hit approximately US$ 8,500 million by 2025. A massive global network of 3.2 billion players interacts with these meticulously modeled environments, supported by a 3D gaming technology market valued at over US$ 34.5 billion in 2024. The evolution of the 3D animation software market is therefore directly tied to the innovation happening within 3D modeling.

- Global consumer spending on VR and AR technologies is on track to exceed US$ 72.8 billion by the end of 2024.

- The overall video game industry is projected to achieve a staggering value of approximately US$ 281.77 billion in 2025.

- By 2037, the 3D gaming technology market is forecast to generate revenues exceeding US$ 237.56 billion.

Animated Content Explosion Cements Animation's Leadership in Software Usage

The animation field is the most significant user of 3D animation software market, accounting for a commanding 42.3% market share. This leadership is fueled by the voracious global appetite for animated content, particularly on streaming platforms. In 2024, the animated series "Bluey" captured an astounding 55.62 billion minutes of viewing time on Disney+, while "Moana" led animated films with 13.03 billion minutes. The top 10 animated movies on these platforms collectively drew in billions of viewing minutes, creating an insatiable demand for new productions. Such high consumption rates directly stimulate the growth and innovation within the 3D animation software market as studios race to meet audience expectations.

The immense financial success of animated films at the box office further justifies the segment's dominance. In 2025, the Chinese animated feature "Ne Zha 2" shattered records, becoming the highest-grossing animated movie ever with US$ 2.2 billion globally. Similarly, "Inside Out 2" earned nearly US$ 1.7 billion worldwide, demonstrating the massive commercial appeal of animated stories. Even live-action adaptations like "Lilo & Stitch," which depend heavily on 3D animation, achieved monumental success, earning US$ 481.8 million domestically to become the number one movie of the summer in 2025. This consistent profitability ensures a robust and continuous demand for the software that brings these creations to life.

- In 2024, "Family Guy" and "Bob's Burgers" also attracted huge audiences on Hulu, with 42.44 billion and 36.80 billion minutes watched.

- The photorealistic 3D animation of the live-action "The Lion King" (2019) helped it earn US$ 1.65 billion globally.

- Demonstrating the power of animated franchises, "Frozen II" grossed an impressive US$ 1.45 billion at the worldwide box office.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Media and Entertainment's Creative Demands Propel Animation Software Growth

The media and entertainment industry is the largest end-user segment, holding a substantial 40.4% share of the 3D animation software market. Its dominance is a direct consequence of the sector's profound reliance on visual effects (VFX) and computer-generated imagery (CGI) to produce compelling content for film, television, and gaming. In 2024 alone, over 1,200 major film and series productions integrated VFX, with specialized software handling 80% of all the effects created. This extensive usage is backed by enormous financial commitments, including a global spend of US$ 120 billion on streaming content production in 2024, much of which funds projects rich in 3D animation.

The video game sector is a particularly powerful engine for the 3D animation software market, with industry revenues hitting US$ 184 billion in 2023 and projected to reach an incredible US$ 455 billion in 2024. Mobile gaming alone is expected to contribute over US$ 98.7 billion. Simultaneously, streaming powerhouses are fueling demand through massive content investments. The top six global content providers, including Disney and Netflix, collectively spent US$ 126 billion on content in 2024. A significant portion of this investment is dedicated to animated features and VFX-heavy series, making the entertainment industry the primary driver of software innovation and adoption.

- The U.S. market for VFX software alone was valued at a significant US$ 975 million in 2024.

- Disney’s estimated content budget for 2024 stands at a massive US$ 35.8 billion.

- Netflix is set to increase its content budget in 2025, building on its 2024 expenditure of US$ 16 billion.

To Understand More About this Research: Request A Free Sample

Regional Analysis

North America Commands Global Animation Through Production and Technological Investment

North America spearheads the global 3D animation software market, holding a commanding share of over 38.20%. This dominance is built on a foundation of massive content creation and deep technological investment. In the United States, the film and entertainment sector remains a primary driver, with the U.S. box office for animated features surpassing US$ 1.5 billion in 2024. The talent ecosystem is robust, with over 12,000 students graduating from animation-related programs in the U.S. in 2024. Furthermore, California's animation and VFX industry supports more than 75,000 jobs. Canada complements this with strong government support, providing over US$ 200 million in federal and provincial tax credits to the animation sector in 2024.

The region's leadership in the global 3D animation software market also stems from its role as an innovation hub. U.S.-based venture capital firms invested over US$ 950 million into startups developing AI-powered 3D creation tools in 2024. The U.S. Department of Defense allocated contracts worth US$ 1.2 billion for advanced simulation and training software. In the industrial space, more than 4,000 digital twin projects were initiated by U.S. manufacturing firms in 2025. The Canadian gaming industry also contributes significantly, employing over 35,000 full-time professionals. Additionally, more than 500 feature films and episodic series in the U.S. utilized virtual production workflows in 2024. The average salary for a senior 3D artist in major U.S. tech hubs reached US$ 135,000 in 2025, attracting top global talent.

Asia Pacific Rises as a Global Content Production and Gaming Powerhouse

The Asia Pacific 3D animation software market is a dynamic force, fueled by its massive consumer markets and unparalleled content production capabilities. Japan's anime industry produced over 300 new television series and films in 2024, driving global demand. South Korea’s gaming sector continues its ascent, with the country's top 5 game developers launching over 40 new titles for global markets in 2024. India has solidified its position as a leading outsourcing hub, with Indian VFX and animation studios securing contracts for over 150 international projects.

China's domestic 3D animation software market is also booming, with its top 10 animated films in 2024 collectively hiring over 20,000 animators. The Chinese government further stimulated growth by investing US$ 3 billion into its national metaverse and digital content initiatives in 2025, while South Korea's Ministry of Culture provided grants totaling US$ 75 million to support independent game developers.

Europe Champions Artistic Animation and Specialized Industrial Simulation Applications

Europe's 3D animation software market is defined by strong government support for creative industries and deep integration of 3D simulation in its advanced manufacturing sectors. The UK's animation industry benefited from over US$ 250 million in tax relief in 2024, supporting more than 60 new animated productions. France remains a cultural hub, with the Annecy International Animation Film Festival showcasing over 500 unique animated projects in 2024. The French government also provided subsidies worth US$ 90 million for video game development. Germany's world-leading automotive industry is a key driver, with the top 3 German automakers collectively employing over 15,000 simulation engineers in 2025. European collaboration is strong, with over 80 international co-productions funded through the Eurimages support fund in 2024. The region’s gaming scene is also thriving, with over 1,200 new game development studios established across the EU in the same year.

Recent Developments in 3D Animation Software Market

- Luma AI Raises US$ 43 Million (June 2024): The generative AI company secured Series B funding to advance its text-to-3D model, Genie, aiming to make 3D creation more accessible.

- Autodesk Acquires Wonder Dynamics (May 2024): Autodesk acquired the AI-powered animation startup to integrate its Wonder Studio, which automates VFX and character animation, into its software suite.

- Leonardo.Ai Raises US$ 47 Million (November 2024): The generative AI content platform secured new funding to expand its suite of tools, which includes image and 3D texture generation capabilities.

- Move AI Raises US$ 10 Million (October 2024): The AI motion capture startup, which enables markerless mocap from video, secured Series A funding to expand its enterprise and creator-focused offerings.

Top Players in 3D Animation Software Market

- SideFX

- The Foundry Visionmongers Ltd

- Qualcomm Technologies, Inc.

- pmdtechnologies ag

- Autodesk Inc.

- AutoDesSys, Inc.,

- Corel Corporation

- EIAS3D

- MAXON COMPUTER GMBH

- Adobe

- NewTek, Inc.

- NVIDIA Corporation

- 3Corus Entertainment Inc.

- Other Prominent Players

Segmental Overview of the Global 3D Animation Software Market

By Deployment

- On-Premises

- Cloud-Based

By Technology

- 3D Modelling

- Motion Graphics

- 3D Rendering

- Visual Effects

- Others

By Application

- Animation Field

- Media Field

- Construction Field

- Others

By End-Users

- Media & Entertainment

- Construction & Architecture

- Healthcare & Lifesciences

- Fashion & Textile

- Education & Research

- Others

By Region

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- The UK

- Germany

- France

- Italy

- Spain

- Poland

- Russia

- Rest of Europe

- Middle East & Africa (MEA)

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- Asia-Pacific

- China

- India

- Japan

- Australia & New Zealand

- ASEAN

- Rest of Asia Pacific

REPORT SCOPE

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | US$ 19.06 Billion |

| Expected Revenue in 2033 | US$ 53.28 Billion |

| Historic Data | 2020-2023 |

| Base Year | 2024 |

| Forecast Period | 2025-2033 |

| Unit | Value (USD Bn) |

| CAGR | 12.1% |

| Segments covered | By Deployment, By Technology, By Application, By End-Users, By Region |

| Key Companies | SideFX, The Foundry Visionmongers Ltd, Qualcomm Technologies, Inc., pmdtechnologies ag, Autodesk Inc., AutoDesSys, Inc., Corel Corporation, EIAS3D, MAXON COMPUTER GMBH, Adobe, NewTek, Inc., NVIDIA Corporation, 3Corus Entertainment Inc., Other Prominent Players |

| Customization Scope | Get your customized report as per your preference. Ask for customization |

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |